Now that we are past the rush of summer and the deluge of news and product introductions that CEDIA Expo brings us, let’s take a moment to take stock of where we are as an industry in terms of how much business we’ve been doing, as well as what kinds of products — and in what quantities — we are selling.

As we have done for the past five years, we have teamed up with Portal.io to share this information, along with a second viewpoint from D-Tools’ data (see sidebar) and the distributor’s view from ADI Global Distribution. As we did last year, this year’s Portal-provided data looks only at closed/won projects, as the focus is on real market insights (what’s being sold).

Flashback: The State of the Industry 2023

Once again providing analysis is Josh Willits, COO of Portal, who is joined this year by a new member of his team, Lee McDonald. McDonald joined Portal.io in February of this year as director of vendor services, having previously run the analytics division for the Nationwide Marketing Group.

The Big Picture

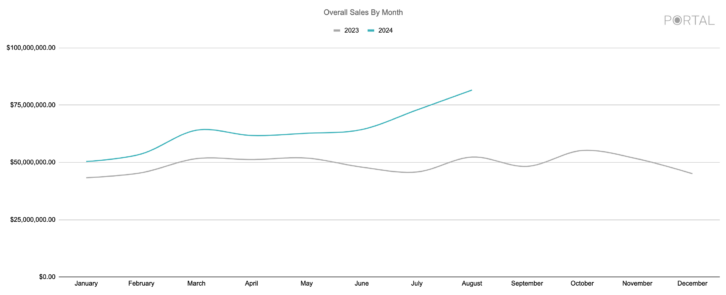

Let’s begin with a look at Figure 1, which shows overall sales by month. Sales are up throughout, with 2024 holding pretty consistent to 2023 through May, and then a sizeable increase heading into August.

“Basically, in the last two quarters of 2023, overall sales by month stagnated and dropped a bit in December,” says Willits. “We’re not seeing that same trend in 2024. My data is showing that the average accepted project volume per month per dealer is up 25% when comparing 2023 to 2024 through August.”

The number of jobs/month also increased from 6.1 jobs/month from January through August 2023 to 6.8 jobs/month during that same time period in 2024, which is an increase of 8.4 jobs/year.

Top Prods

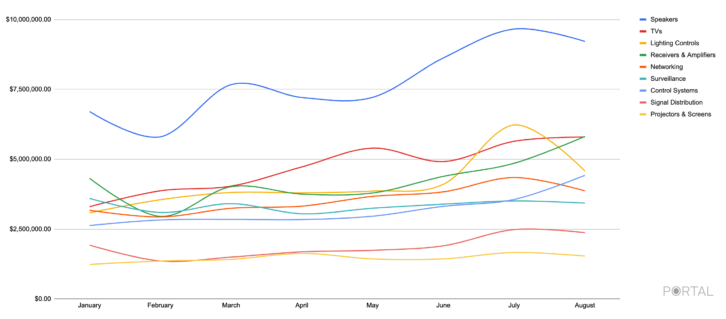

In Figure 2, we can see the top-selling categories, with Speakers taking the top spot for another year. “There was not much shuffling in the top products this year,” says Willits. “Of the top categories, Networking is fairly stagnant, while clearly Control is not in decline, as some have recently suggested. Signal Distribution — another category said to be in decline — saw some growth as well, possibly because there’re more options for distributed audio for dealers such as Media over IP and Dante.”

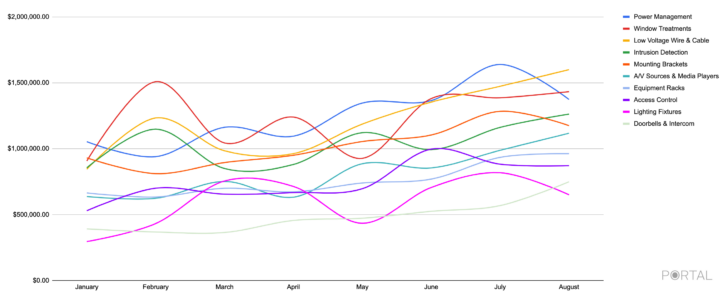

The secondary products are covered in Figure 3, which offers some interesting findings.

“February has a dip across categories in both the top products and the second-tier ones,” says Willits. “However, there was an increase in window treatments, bulk wire, and a few of the security products — all categories that are generally associated with longer-term projects. So, what we’re seeing here is a February drop in category sales that we did not see in dealer overall sales.

“We’re seeing a dip in February sales in categories that dealers place orders when they close the job, so manufacturers would feel that while the dealer would not. Dealers were still doing business in February, but they just weren’t ordering.”

In terms of secondary categories on the move, Power Management has taken the lead for the year, with month-over-month growth for the category with the exception of August.

Hot Categories

Unsurprisingly, Lighting and Shades have shown noteworthy growth year over year. Figure 4 shows Lighting Fixture sales from January 2023 through August 2024, and while the growth is not as much as it was from 2022 to 2023, it is still significant.

“What’s interesting is it looks like there were some ups and downs through 2023, but the year finished down slightly from where it started,” says McDonald. “But this year has seen an increase in sales by almost half a million dollars, which is pretty remarkable.”

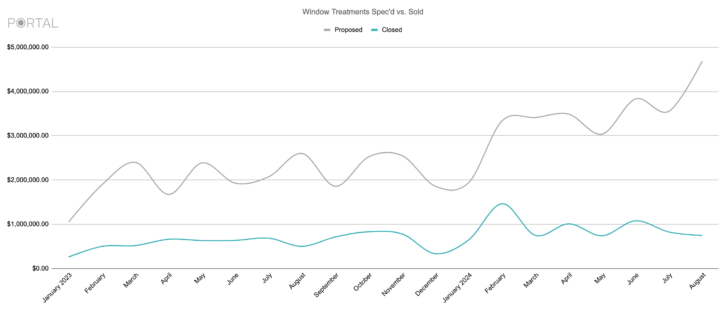

Figure 5 takes a look at the dollar amount of window treatments specified vs. sold, and the increase in spec’d shades in 2024 is staggering.

“The difference between proposed versus sold jumps, so we’re seeing a lot more window treatments being included on proposed systems,” says Willits. “The data shows that more dealers are spec’ing shades, which tells us that shades have a higher mindshare with dealers than in 2023. The adoption, at least for including on proposals, is increasing.”

The Distributor’s View

Cynthia Menna, VPGM AV at ADI Global Distribution, provides some insights into the best-selling product categories and current industry trends experienced by the company:

“New growth opportunities continue to emerge across the residential AV market thanks to new product innovations, as well as elevated end-user expectations and consumer demands,” says Menna. “Consumers want flexible, convenient, smart, and intuitive solutions that help enhance everyday life by making it simpler, more fun, and a lot more connected. Manufacturers and distributors alike are going above and beyond to help meet these evolving needs.

“Aligning with the trend toward smarter and more connected homes, seamless integration across the home has become even more important. Installers recognize the need to provide customizable solutions tailored to their customers. From security, AV, lighting controls, shades, temperature controls, video doorbells, and beyond, homeowners understand the value of these technologies and are ready to invest in their homes.

“Whether enhancing movie nights or gaming sessions, integrators are using the latest technologies to create engaged and inviting experiences across the home. Products driving these installations — TVs, projectors, speakers, soundbars, wireless audio, amplifiers, IoT, streaming services, 4K content, and beyond — continue to drive growth across the category.

“Outside entertainment continues to drive growth as smart technologies are used to transform patios and backyards into immersive, connected spaces for relaxation and fun. With our combined business (ADI and Snap One), we’re helping to bring more of these brands that offer durable and all-weather designs, like SunBrite TVs and Episode Surroundscape speakers, to integrators so they can make these dreams become reality for end customers.

“’Resimercial’ has become a standard industry term as residential integrators are completing more light commercial work. And they’re leaning on their distributors and manufacturer partners for the products, training, and support to help make this happen. From digital signage and audio distribution to video conferencing and automation, we’re helping them expand their offerings and capitalize on new revenue opportunities across commercial customers.

“As a new combined business, ADI and Snap One is committed to providing our customers with a comprehensive product portfolio and strong exclusive brands roadmap to help them succeed in today’s market. We’re looking forward to bringing the best of each company together to deliver more products and services, more buying convenience, and more local expertise and support.”

Conclusion

Business seems to be holding steady, with opportunities coming in from expansion product categories such as lighting and shades and trends such as outdoor entertainment and light commercial work.

Here’s to crushing the last quarter!

For more detailed, brand-specific sales data, manufacturers and distributors can contact josh@portal.io.

D-Tools Data: Are Integrators Facing a Self-Perpetuating Cycle of Harder Work?

By Jason Knott, Data Solutions Architect & Evangelist, D-Tools

For many integrators, it might feel like they are working a lot harder just to maintain the same amount of business, and recent data from D-Tools verifies that is exactly the situation. According to the D-Tools 2024 Midyear Market Report, integration companies are having to produce significantly more proposals just to maintain the same number of installation projects, while at the same time fighting increased costs for products and labor.

The entire situation is potentially creating a self-perpetuating cycle that feeds upon itself. Here’s how it goes: As inflation continues to occur, prices go up. When integrators have to pay more for products and labor, they have to charge their clients more. When those customers balk at the higher price tags, they either scale back the project scope or resist signing the contract at all. When integrators are faced with increased value engineering and lower closing rates, they have to generate more proposals just to maintain the same level of revenue and profit. When that happens, everyone is working at a frantic pace. Is that cycle of activity sustainable over the long haul? Who knows.

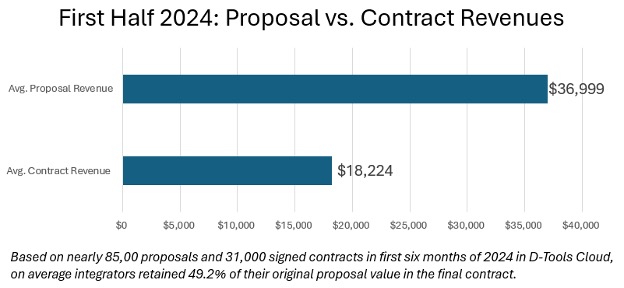

Specifically, the data is drawn from nearly 85,000 proposals and nearly 31,000 signed contracts originated in D-Tools Cloud for the first half of 2024 for both residential and commercial projects. In general, it reveals that integrators are indeed producing more proposals at a much higher average price, but executing roughly the same number of installations. [Note: The exact split between residential and commercial projects is not broken out in the D-Tools 2024 Midyear Market Report; however, in 2023 commercial projects were on average 37% larger in terms of revenue than residential installations.]

Comparing the first six months of 2024 to the first half of 2023:

- The average number of proposals grew nearly 9% to 85 proposals, or about 14 per month per integrator.

- The average number of signed contracts grew 3.7% to 44 contracts, or about 7 per month per integrator.

- The average signed contract value rose a whopping 19.6% to $18,224.

The data initiates a slew of questions and possible conclusions. First, the growing number of proposals means demand remains strong for professional installation. That’s good — it means the market is healthy. While housing starts have been up and down, integrators indicate anecdotally that the luxury end of the market remains very strong.

Another plausible explanation as to why integrators are cranking out more proposals could be due to the ease of using software such as D-Tools. What might have taken them hours to produce in the past can now be done in a fraction of the time. Lastly, the proposal growth could be due to the bounce back in the commercial market that was devastated by the worldwide Covid-19 pandemic.

But if the number of proposals is up, why aren’t the number of signed contracts correspondingly up by the same percentage rate? The average number of signed contracts by integrators rose only slightly in the first half of 2024 compared to the previous year. We can speculate that customers are being gun shy due to economic and political uncertainty, and it could be that the market in general is more competitive with more security contractors and electricians branching into the smart home world.

Meanwhile, the data from the D-Tools 2024 Midyear Market Report, which is available as a free download on www.d-tools.com, reveals that only 52% of proposals that are being presented to customers are ultimately being converted into contracts. That is down from 55% over the previous two years. The lower closing rate seems to affirm that competition could be getting more fierce. Moreover, when customers do eventually sign the contract, it has been value engineered or “de-scoped” down by 51% on average from the original proposal value. So, think about it…the average integrator is only closing half of their proposals and likewise only maintaining half of the proposal dollars in the final contract. Yikes!

On a positive note, contract sizes are up, as noted. And while inflation certainly is responsible for much of that increase, it is also an indicator that integrators are aggressively expanding into new product categories, such as lighting fixtures, electrical, and power. That diversification is good for the market and the wallet, especially when the general economy and political climate are causing clients to delay decisions and push back projects.

Looking ahead, in 2023 the second half of the year was very strong with integrators. According to the various buying groups, pipelines look solid for the rest of the year and into 2025. One thing is for certain as the industry heads into the final quarter of 2024 and begins planning for 2025: Integrators are working harder than ever before.

Portal.io Uses AI to Help Build Proposals

Optimisitc pundits claim that articifical intelligence won’t take jobs away from people, but enable them to do their jobs easier, faster, and better. Portal pushed the CI industry closer to that conclusion with its new AI Proposal Builder that can create a propsal from a video walkthrough of a project. Demonstrations of this technology kept the Portal booth packed at CEDIA Expo and earned it a Best of Show award from Residential Systems.

To use it, dealers simply record a video walkthrough of the project or dictate a project spec during their drive back to the office and they will have a proposal waiting for them by the time they arrive. Leveraging more than a million historical proposals, Portal’s AI Proposal Builder will process video, audio, and text-based project specification files and generate a complete proposal using dealer preferred items and prices.

Visit portal.io to schedule your own demonstration.